Keynesian Versus Classical Long-run AS

- Long run aggregate supply (LRAS) is influenced by a change in the productive capacity of the economy

- Productive capacity is changed by changes to the quantity or quality of the factors of production

- Economists have two opposing views on how LRAS works in an economy

- The original view is called the classical view

- The insights developed by John Meynard Keynes in 1936 are called the Keynesian view

The Classical LRAS View

- The classical view believes that the LRAS is perfectly inelastic (vertical) at a point of full employment of all available resources

- This point corresponds to the maximum possible output on a production possibilities frontier (PPF)

- This point corresponds to the maximum possible output on a production possibilities frontier (PPF)

- The classical view believes that in the long-run an economy will always return to this full employment level of output

- There may be short-run output gaps in the economy

- During extreme periods of economic growth there can be an inflationary gap that develops

- In the long run this will self-correct and return to the long-run level of output, but at a higher average price level

- During slowdowns or recessions there can be a recessionary gap that develops

- In the long-run this will self-correct and return to the long-run level of output, but at a lower average price level

- During extreme periods of economic growth there can be an inflationary gap that develops

A diagram that shows the Classical View of long-run aggregate supply (LRAS) with a vertical aggregate supply curve at the full employment level of output (YFE)

Diagram Analysis

- Using all available factors of production, the long-term output of this economy (LRAS) occurs at YFE

- The economy is initially in equilibrium at the intersection of AD1 and LRAS (P1, YFE)

- A slowdown reduces output from AD1→AD2 and creates a short term recessionary gap

- This self corrects in the long term and returns the economy to the long-run equilibrium at the intersection of AD2 and LRAS (P2, YFE)

The Keynesian LRAS View

- Keynes believed that the long-run aggregate supply curve (LRAS) was more L shaped

- Supply is elastic at lower levels of output as there is a lot of spare production capacity in the economy

- Struggling firms will increase output without raising prices

- Supply is perfectly inelastic (vertical) at a point of full employment (YFE) of all available resources

- The closer the economy gets to this point the more price inflation will occur as firms compete for scarce resources

- The closer the economy gets to this point the more price inflation will occur as firms compete for scarce resources

- Supply is elastic at lower levels of output as there is a lot of spare production capacity in the economy

- The Keynesian view believes that an economy will not always self-correct and return to the full employment level of output (YFE)

- It can get stuck at an equilibrium well below the full employment level of output e.g. Great Depression

- It can get stuck at an equilibrium well below the full employment level of output e.g. Great Depression

- The Keynesian view believes that there is role for the government to increase its expenditure so as to shift aggregate demand and change the negative 'animal spirits' in the economy

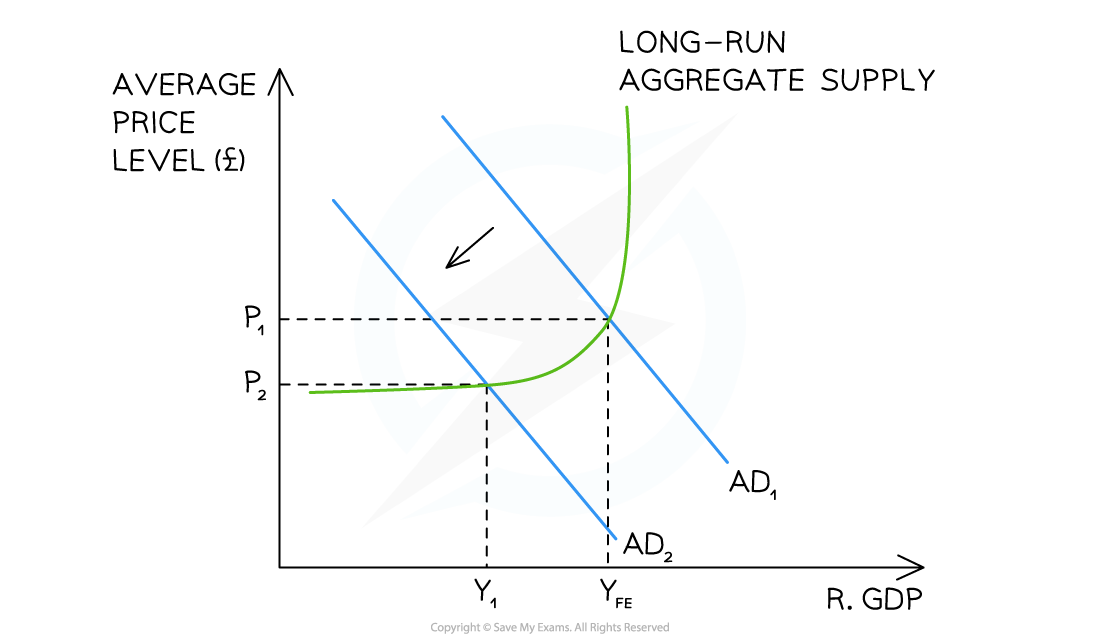

A diagram that shows the Keynesian View of long-run aggregate supply (LRAS) with a vertical aggregate supply curve at the full employment level of output (YFE) becoming more elastic at lower levels of output

Diagram Analysis

- Using all available factors of production, the long-term output of this economy (LRAS) occurs at YFE

- The economy is initially in equilibrium at the intersection of AD1 and LRAS (P1, YFE)

- A slowdown reduces output from AD1→AD2 and creates a recessionary gap Y1-YFE

- The economy may reach a point where average prices stop falling (P2), but output continues to fall

- This economy may not self-correct to YFE for years

- The low output leads to high unemployment and low confidence in the economy

- This stops further investment and further reduces consumption

- This stops further investment and further reduces consumption

- Keynes argued that this was where governments needed to intervene with significant expenditure e.g. Roosevelt's New Deal; response to financial crisis of 2008